I. Background: Increasing Compliance Challenges in Cross-Border Service Transactions #

With the continuous implementation of China’s “Going Global” strategy, cross-border service transactions between Chinese enterprises and overseas entities or individuals have become increasingly common. The proper declaration and payment of value-added tax (VAT) and related tax obligations under domestic law has become a pressing compliance concern, especially in industries such as foreign trade, manufacturing, and the internet economy.

Key compliance issues include:

- Whether overseas services constitute VAT-taxable activities within China;

- Whether the Chinese party must act as a withholding agent;

- Whether withheld VAT can be claimed as input tax credit.

This article provides a systematic overview of VAT treatment for outbound service fee payments, under the framework of the new Value-Added Tax Law of the People’s Republic of China (effective from 2026-01-01), supplemented by applicable regulations, circulars, and practical guidelines.

II. Determining VAT Liability: Does the Transaction Constitute a Domestic Taxable Activity? #

- Legal Basis

Article 4(4) of the VAT Law of the People’s Republic of China (effective 2026-01-01):

“A taxable transaction within the territory includes the following: (…) (4) for the sale of services or intangible assets, if the service or asset is consumed within the territory, or the seller is a domestic entity or individual.”

Article 1 of the Interim VAT Regulations (2017 Revision):

“Any entity or individual that sells services within the territory of the People’s Republic of China shall be deemed a VAT taxpayer and shall pay VAT accordingly.”

Article 13(1) of the Pilot Implementation Measures for Replacing Business Tax with VAT (Caishui [2016] No. 36):

“The following shall not be deemed as domestic sales of services or intangible assets: (1) services fully rendered outside China by a foreign entity or individual to a domestic entity or individual.”

- Practical Standard: “Domestic Consumption” Test

The key factor is whether the service is ultimately consumed within China. Common evaluation criteria include:

| Service Type | Domestic Consumption | Practical Indicator |

| Overseas advertising targeting China | Yes | Target audience located in China |

| Foreign technical consulting used in China | Yes | Deliverables applied in domestic operations |

| Foreign legal services for offshore arbitration | No | Services used in foreign legal proceedings |

| Software licensing deployed on China-based servers | Yes | End-use within China |

Similar judging standard refer to Caishui [2016] No. 36 (Annex 4) and STA Announcement [2016] No. 29 for rules on zero-rating or exemption for cross-border VAT-liable activities.

III. Is the Chinese Party Required to Withhold VAT? #

- Legal Basis

Article 15 of the VAT Law (effective 2026-01-01):

“Where an overseas entity or individual engages in a taxable transaction within the territory, the purchaser shall act as the withholding agent, unless a domestic agent is appointed to file and pay taxes on its behalf pursuant to State Council regulations.”

Article 18 of the Interim VAT Regulations (2017 Revision):

“Where an overseas entity or individual sells services within China without establishing a domestic business presence, its domestic agent shall act as the withholding agent. If no agent exists, the purchaser shall act as the withholding agent.”

- Conditions for Withholding Obligation

Chinese enterprises must fulfill the VAT withholding obligation if the following three conditions are met:

The service provider is an overseas entity or individual;

The service is consumed or utilized within China;

The overseas party has no business presence in China or has not registered for tax purposes in relation to the service activity.

In such cases, the Chinese payer must withhold VAT at the time of payment and declare and remit the tax to the competent tax authority.

IV. Can Withheld VAT Be Claimed as Input Credit? #

- Legal Basis

Article 22(4) of the VAT Law (effective 2026-01-01):

“Input VAT shall not be creditable if related to goods, services, intangible assets or real estate purchased for collective welfare or personal consumption.”

Article 8(2)(4) of the Interim VAT Regulations (2017 Revision):

“Input VAT may be credited for the purchase of services, labor, intangible assets, or real estate from an overseas entity or individual, provided that the VAT amount is shown on a withholding tax certificate issued by the tax authority or withholding agent.”

- Conditions for Input VAT Credit

To claim withheld VAT as input tax, the enterprise must:

Be registered as a general VAT taxpayer;

Obtain a valid withholding tax payment certificate;

Use the service exclusively for taxable business activities, not for personal or collective welfare use.

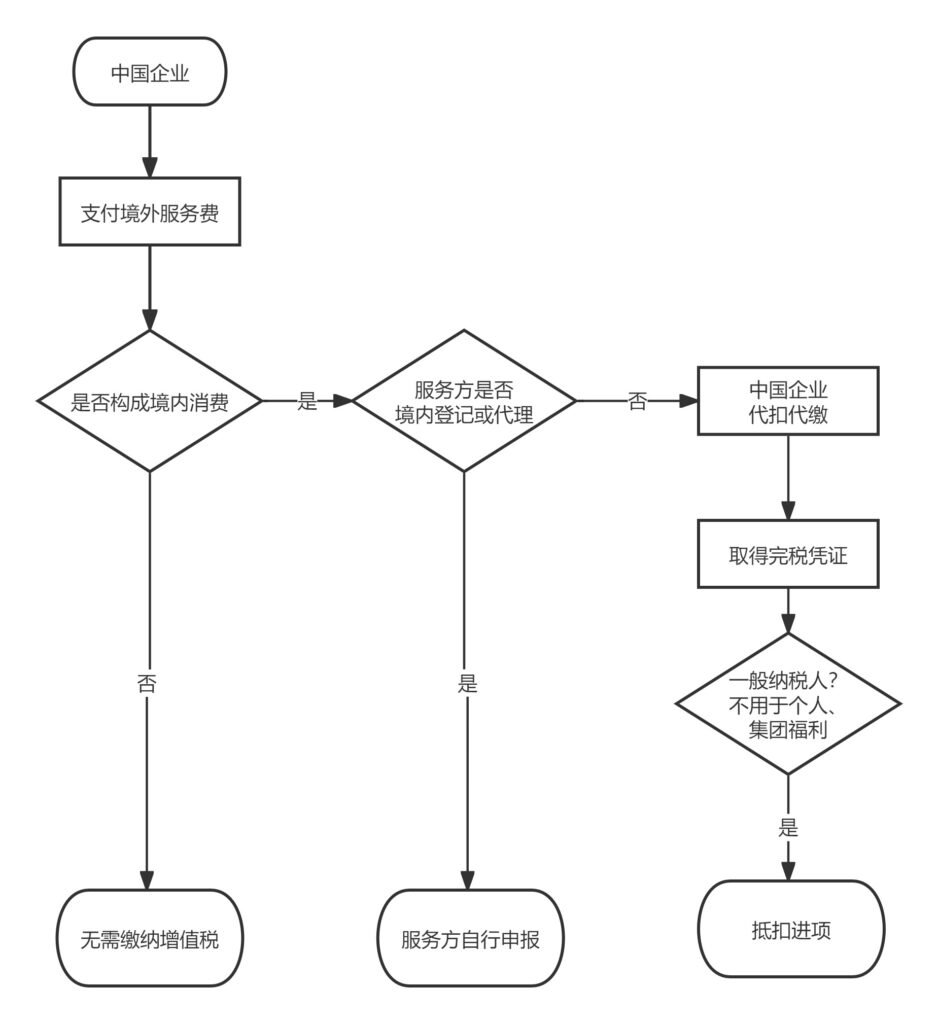

V. Decision-Making Flowchart for Cross-Border VAT Treatment #

A visual process chart can be inserted here to guide enterprises in evaluating VAT obligations based on the type, location, and use of the service.

This article is for informational purposes only and does not constitute legal advice. For case-specific consultation, please contact us. Read our full Legal Disclaimer, which also includes information on translation accuracy.