I. Background: Strengthening Tax Risk Control for Agency-Based Exports #

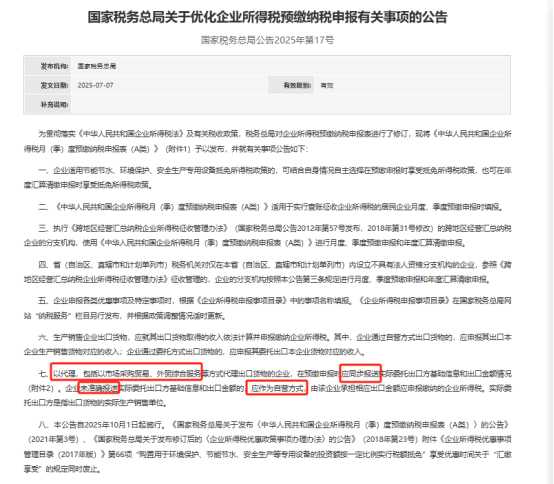

On 2025-07-07, the State Taxation Administration (STA) issued the Announcement on Optimizing Corporate Income Tax Prepayment Filing Procedures (STA Announcement [2025] No. 17, hereinafter “Circular No. 17”), which will come into effect on 2025-10-01.

Article 7 of Circular No. 17 further clarifies the boundaries between agency-based exports and self-operated exports for corporate income tax (CIT) purposes. It aims to standardize CIT prepayment filings and reinforce regulatory oversight over the recognition of agency income and the identification of the appropriate taxpaying entity.

The Circular carries particular significance for enterprises engaged in agency models such as 1039 Market Procurement Trade and Integrated Foreign Trade Services (IFTS).

II. Key Regulatory Changes and Filing Requirements (Applicable from 2025-10-01 Onward) #

1. Declaration of Taxable Revenue Limited to “Agency Service Fees”

Circular No. 17 mandates that export agents may only report agency service fees as taxable revenue when filing for CIT prepayment.

Example: If an export agent charges RMB 100,000 in service fees from the actual domestic consignor, only this amount shall be subject to CIT.

2. Mandatory Submission of the “Summary Table of Entrusted Export by Agency Enterprises”

Export agents must submit the Summary Table of Entrusted Export by Agency Enterprises during the CIT prepayment period, truthfully and completely disclosing the following information:

- Customs declaration number;

- Name of the actual domestic consignor (i.e., the real cargo owner);

- Identification of the cargo owner: either the national ID number (for individuals) or the taxpayer identification number/Unified Social Credit Code (for enterprises or sole proprietors);

- Declared export amount.

This filing obligation is mandatory and serves as a critical basis for tax authorities to verify the authenticity of agency relationships.

3. Failure to Submit or Misreporting May Trigger “Deemed Self-Operated” Treatment

If the agent fails to submit the required information or erroneously reports a non-cargo-owner entity (such as a customs broker or upstream intermediary), the tax authority may deem the transaction to be a self-operated export.

Consequences include:

- Full export value treated as taxable revenue;

- Back taxes and late payment interest imposed.

Such treatment may significantly increase the enterprise’s tax burden and may also trigger further tax audit exposure.

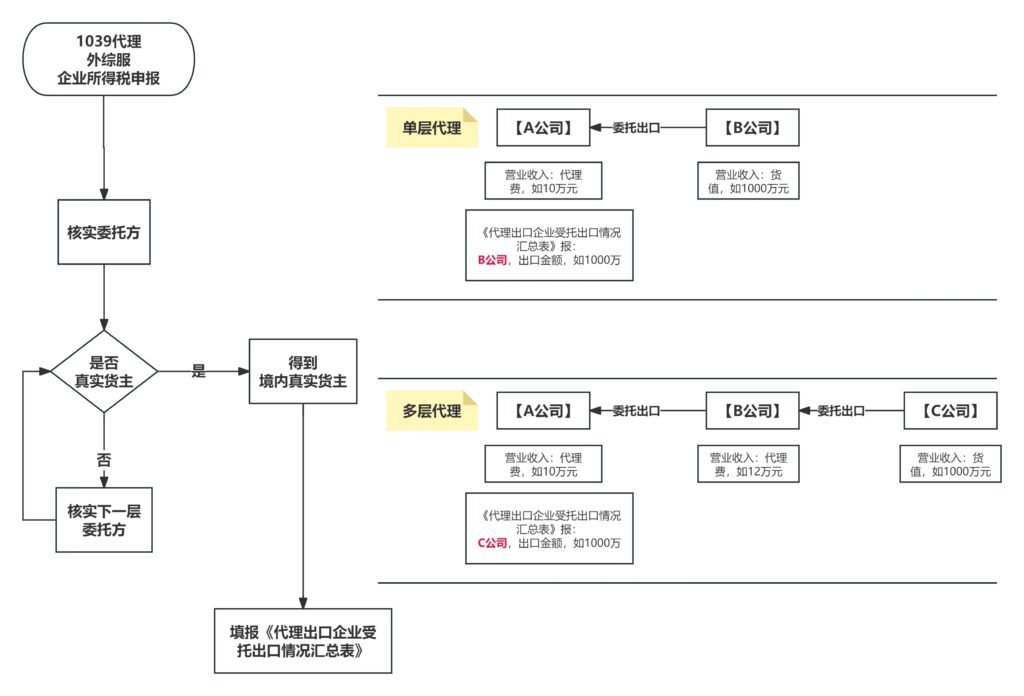

III. Visual Guide: Determining Filing Obligations under Single- and Multi-Tier Agency Structures #

To assist enterprises in determining the appropriate filing path, a reference diagram is provided below.

Agency structures may fall into single-tier or multi-tier delegation models. Regardless of the structure, Circular No. 17 requires that the actual domestic cargo owner be accurately identified and reported in the Summary Table of Entrusted Export. Inaccurate or incomplete filings may result in the agent bearing tax liabilities on the full export amount.

IV. How to Address Transactions Conducted Before 2025-10-01 #

For transactions completed prior to 2025-10-01, enterprises may still rely on existing rules to establish appropriate tax liability attribution.

According to Article 3 of Joint Announcement [2025] No. 8 (issued by the STA, MOF, MOFCOM, GACC, and SAMR), where the enterprise has obtained a valid Certificate of Agency Export of Goods and completed necessary filing procedures, the tax authority may recognize the agency relationship and allow tax liability to be traced to the actual domestic cargo owner.

To mitigate tax risk associated with historical transactions, enterprises are advised to:

- Confirm whether a valid Certificate of Agency Export of Goods has been issued for each transaction;

- Retain all relevant supporting documents (e.g., agency agreements, customs declarations, financial records) for potential audit inspection.

This article is for informational purposes only and does not constitute legal advice. For case-specific consultation, please contact us. Read our full Legal Disclaimer, which also includes information on translation accuracy.